Company Sponsor: Goldbell Financial Services

Goldbell Financial Services (GBFS) is a subsidiary of Singapore’s market leader in industrial vehicles, Goldbell Group, and is currently the preferred financing partner for corporates and individuals for automotive needs. The company offers a range of automotive loans including hire-purchase for commercial, private hire and passenger vehicles, tailored to the needs of its customers.

Title: Developing In-House Credit Scoring System

Project Team: Adam Joshua Lee Jia Hao, Bernice Ong Jingwen, Kevin Wang Weijie, Lim Boon Wen, Ng Hean Kim Nigel and Yan Janice

“How can GBFS enhance its lending decisions for corporate clients using a credit scoring model?” The current corporate loan approval process relies heavily on employee judgement due to the high level of subjectivity in analysis of corporate loans. For example, GBFS often assesses the importance of the vehicle within a business’ context, which differs from client to client. This dependence on manual review causes the loaning process to be extra time-consuming. Through our collaboration with GBFS, our team hopes to introduce analytics and address the issue by combining both the benefits of data analysis and human judgement. With a credit scoring model, our team aims to automate the review of loan applications and flag out certain subjective factors for employee review. This will improve the loaning process, as employees shift their focus to factors that require more human judgement.

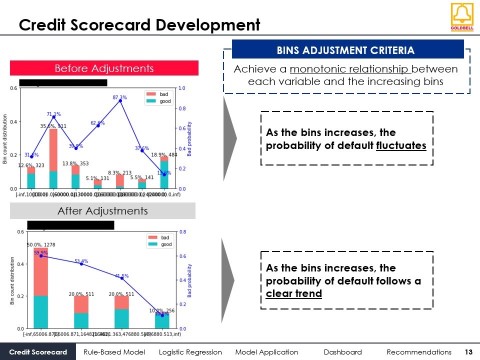

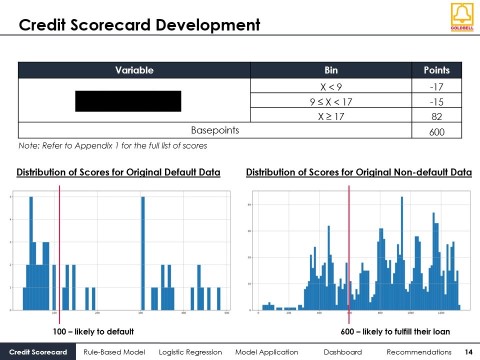

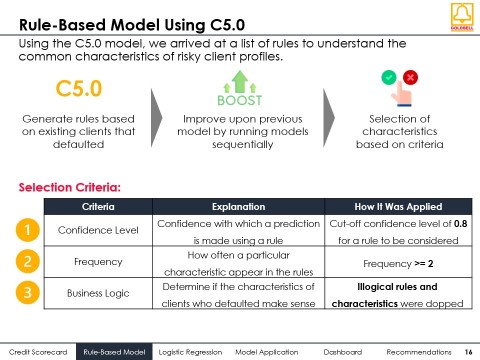

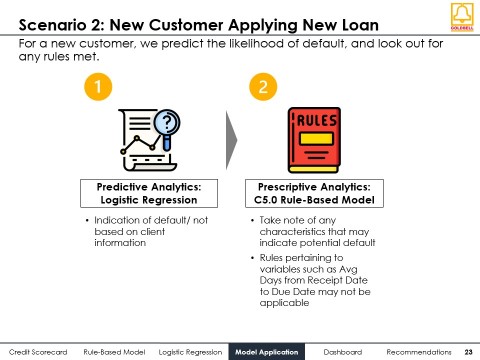

GBFS’ commitment and tight feedback loop assisted our team in developing a credit scoring system tailored to GBFS’ corporate clienteles. This system may be viewed as a three-part model, with both prescriptive and predictive elements. For the prescriptive models based on historical data, statistical methods were employed to analyze the data of past loans and learn about repayment patterns of existing customers. The first model is a credit scorecard system, where each existing corporate client is assigned a credit score, with a higher score indicating lower risk of default historically. The second mode is a classification tree model. Using the C5.0 classification algorithm, key characteristics were identified as indicators of default among existing defaulted loans, suggesting that new loans should be vetted for such characteristics before approval.

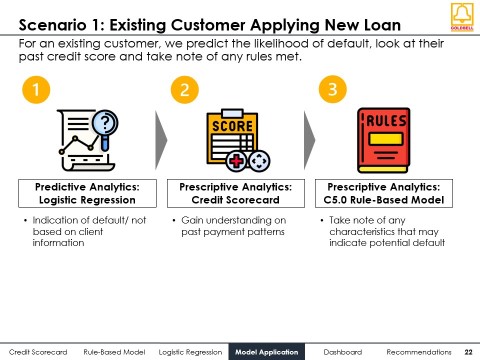

For the third predictive model for new corporate loans, our team used logistic regression to predict the likelihood of default. Bringing everything together, our team presented two scenarios of the loan approval process to GBFS using the models, for new customers, as well as existing customers. To visualize and understand the data better, our team also prepared a Power BI management dashboard showcasing a macro-overview of GBFS’ corporate loans. This dashboard highlights key insights of the existing corporate loans and may be used to demonstrate Goldbell’s capabilities to management, while serving as a pitch deck to potential investors. In an effort of constant improvement, our group concluded the project by sharing some recommendations with GBFS.

Through this capstone project, our team learnt to manage client expectations and communicate effectively. During our meetings with GBFS, whenever we ran into an issue in terms of our technical knowledge or skill, our team made an effort to be transparent and discuss solutions openly. We acknowledged that there were certain areas we were not specialized in (e.g. Integrating the credit scorecard models into the client’s system on the back-end) and remained optimistic yet realistic with the solutions we offered to GBFS. Our team also learnt the importance of updating our client about the project status regularly. This helped us ensure that any adjustments or comments about our progress were aligned with the client’s expectations and minimized any unpleasant ‘surprises’.